Navigating the complexities of credit card debt can feel overwhelming, especially when trying to understand how interest accrues and impacts your repayment journey. Fortunately, tools exist to demystify this process, and a Credit Card Interest Calculator Excel Template stands out as an incredibly effective solution. This practical resource empowers individuals to take control of their finances by visualizing the true cost of their outstanding balances, projecting repayment timelines, and experimenting with different payment strategies to minimize interest paid and accelerate debt freedom. By providing a clear, dynamic model, such a template transforms abstract financial concepts into concrete, actionable insights, helping users make informed decisions about their credit card obligations.

Understanding your credit card interest is not just about knowing your Annual Percentage Rate (APR); it's about seeing how that rate translates into actual dollars and cents over time. Minimum payments, while seemingly manageable, often extend the repayment period significantly, leading to substantial interest charges that can feel like a never-ending cycle. Without a clear projection, it's easy to underestimate the long-term impact of carrying a balance.

This is where the power of an Excel template becomes invaluable. Unlike static online calculators, an Excel template offers flexibility and a deeper level of customization. You can adjust variables, save different scenarios, and integrate it with your broader financial planning. It becomes a personal financial modeling tool, tailored to your specific situation, allowing for a proactive approach to debt management rather than a reactive one.

The goal of this article is to explore the benefits, functionality, and effective use of a credit card interest calculator built in Excel. We'll delve into how these templates work, what features to look for, and how they can be leveraged to accelerate your path to becoming debt-free, ultimately saving you a significant amount of money and financial stress.

Why Use a Credit Card Interest Calculator Excel Template?

Managing credit card debt effectively requires more than just making your minimum payments. It demands foresight, strategic planning, and a clear understanding of how interest charges affect your financial progress. A Credit Card Interest Calculator Excel Template offers a robust solution, providing numerous advantages over simpler tools or manual calculations.

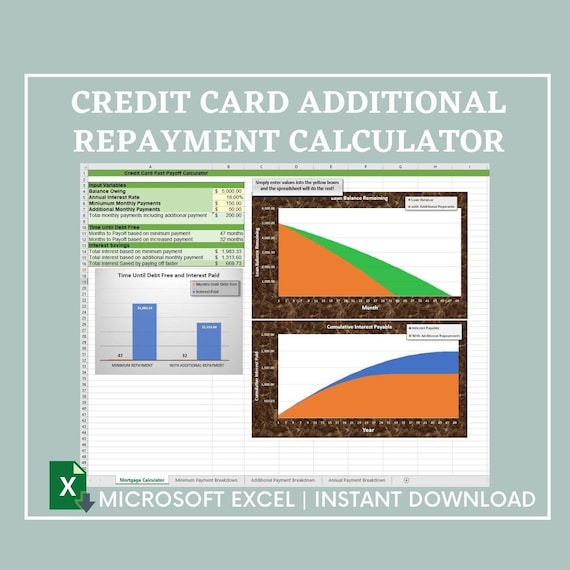

Firstly, it offers transparency. Many people struggle to grasp the true cost of their credit card debt because the interest calculation can seem opaque. An Excel template breaks down the principal and interest components of each payment, showing exactly how much of your money is going towards the original debt versus the cost of borrowing. This clarity is crucial for making informed financial decisions.

Secondly, these templates provide customization and flexibility. Unlike basic online calculators, an Excel template allows you to easily adjust various parameters. You can model different payment amounts, explore the impact of interest rate changes, or even factor in additional lump-sum payments. This dynamic capability enables you to create multiple scenarios and find the optimal strategy for your financial situation. For instance, you can compare a scenario where you pay an extra $50 per month versus an extra $100, immediately seeing the difference in repayment time and total interest paid.

Thirdly, an Excel template serves as a powerful motivational tool. Seeing a clear projection of your debt-free date and the total interest saved by increasing payments can be incredibly motivating. It transforms an abstract goal into a tangible timeline, encouraging consistent effort towards financial freedom. Watching the remaining balance decrease with each projected payment provides a visual representation of progress, which can be a significant boost to your debt repayment journey.

Finally, an Excel template integrates seamlessly with other personal finance spreadsheets. If you're already tracking your budget, savings, or investments in Excel, adding a credit card interest calculator to your suite of tools creates a more holistic financial overview. This integration simplifies data management and provides a centralized hub for all your financial planning needs, making it easier to see how your credit card debt fits into your overall financial picture.

Core Features of a Credit Card Interest Calculator Excel Template

An effective Credit Card Interest Calculator Excel Template should be designed with user-friendliness and comprehensive functionality in mind. While templates can vary, several core features are essential for providing valuable insights into credit card debt repayment.

Key Input Fields

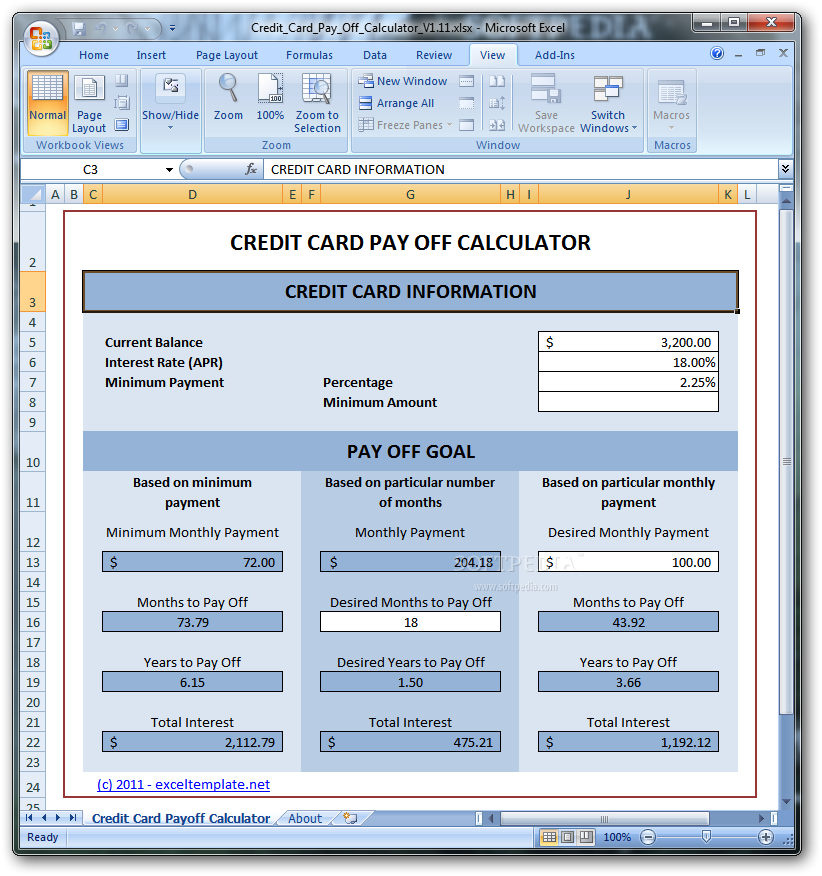

The foundation of any good calculator lies in its input fields. Users should be able to easily enter the following crucial data points:

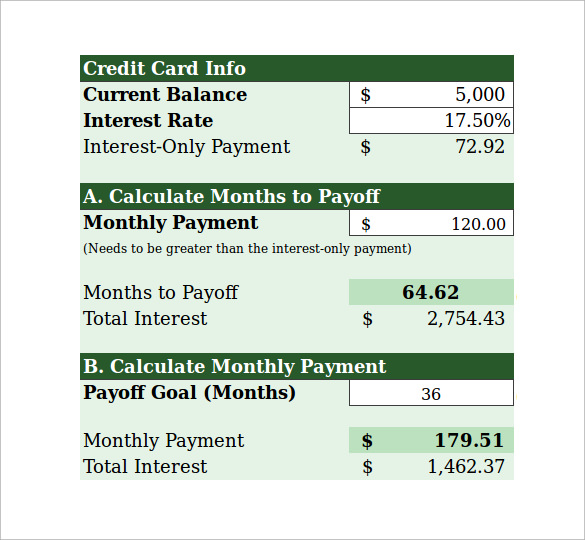

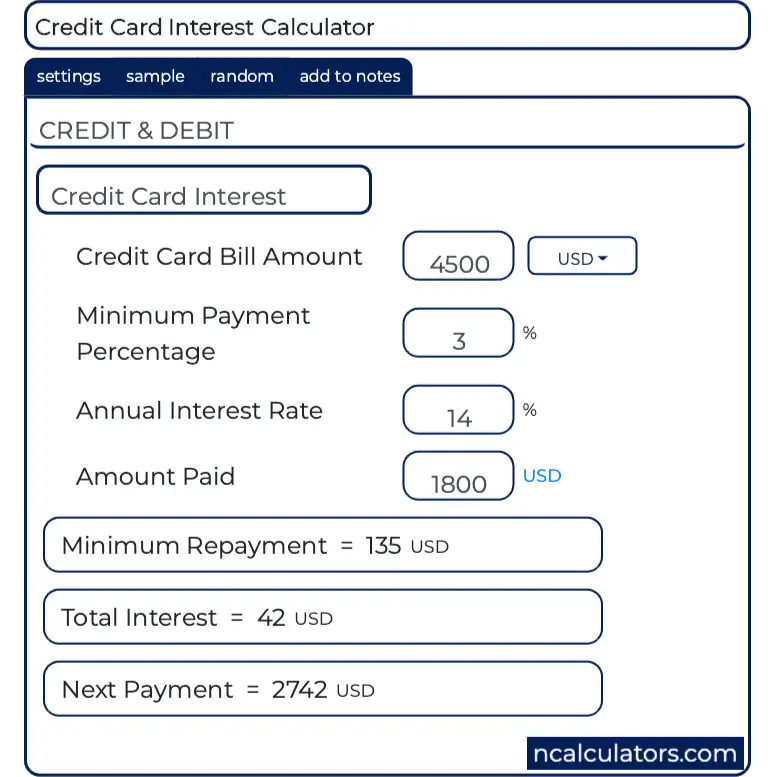

- Current Balance: The total outstanding amount on your credit card.

- Annual Percentage Rate (APR): The interest rate charged by the credit card company, usually expressed as an annual percentage. It's important to use the actual rate, as promotional rates might expire.

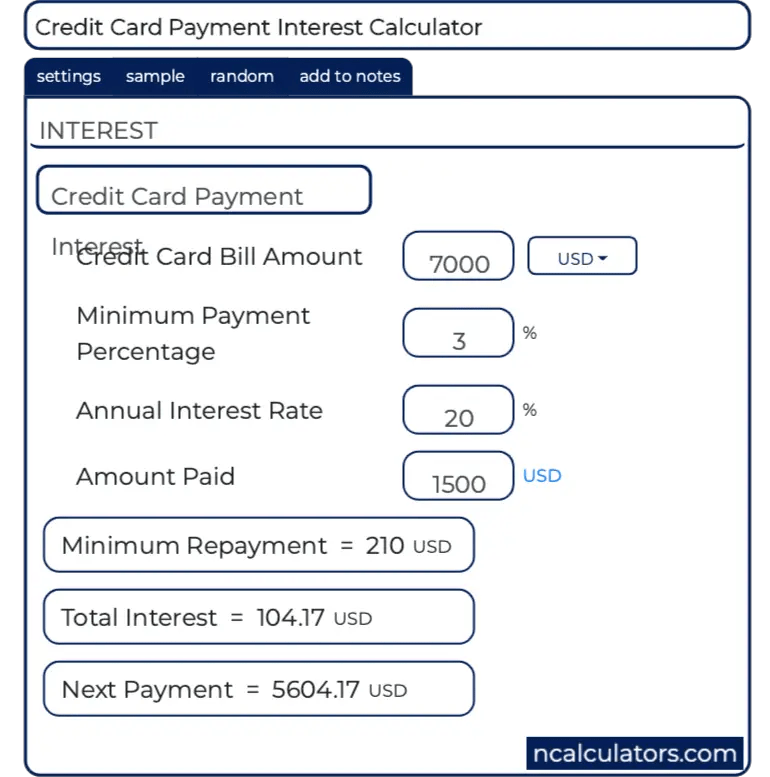

- Minimum Payment: The lowest amount required by your credit card issuer each month. This is often a percentage of the balance or a fixed amount.

- Desired Monthly Payment (Optional): This is where the template becomes powerful. Users can input an amount greater than the minimum payment to see the impact on their repayment schedule and total interest.

- Payment Start Date: To accurately project future payments and the debt-free date.

Calculation Logic and Output

Once the inputs are provided, the template should automatically perform calculations and display clear, actionable outputs:

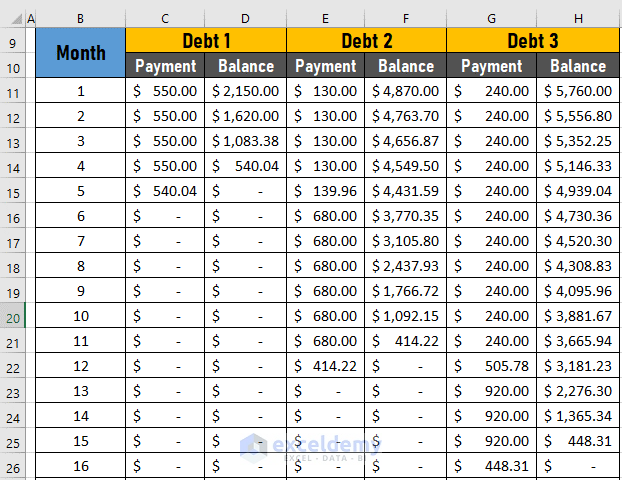

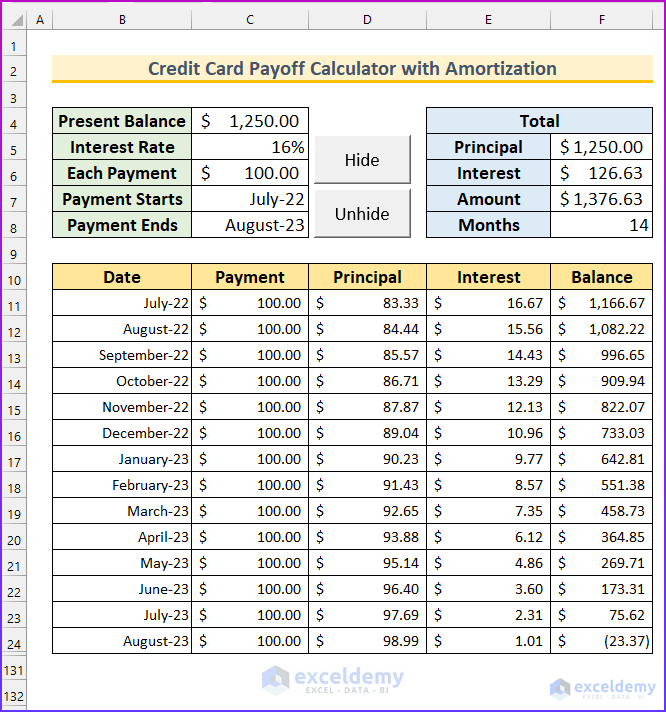

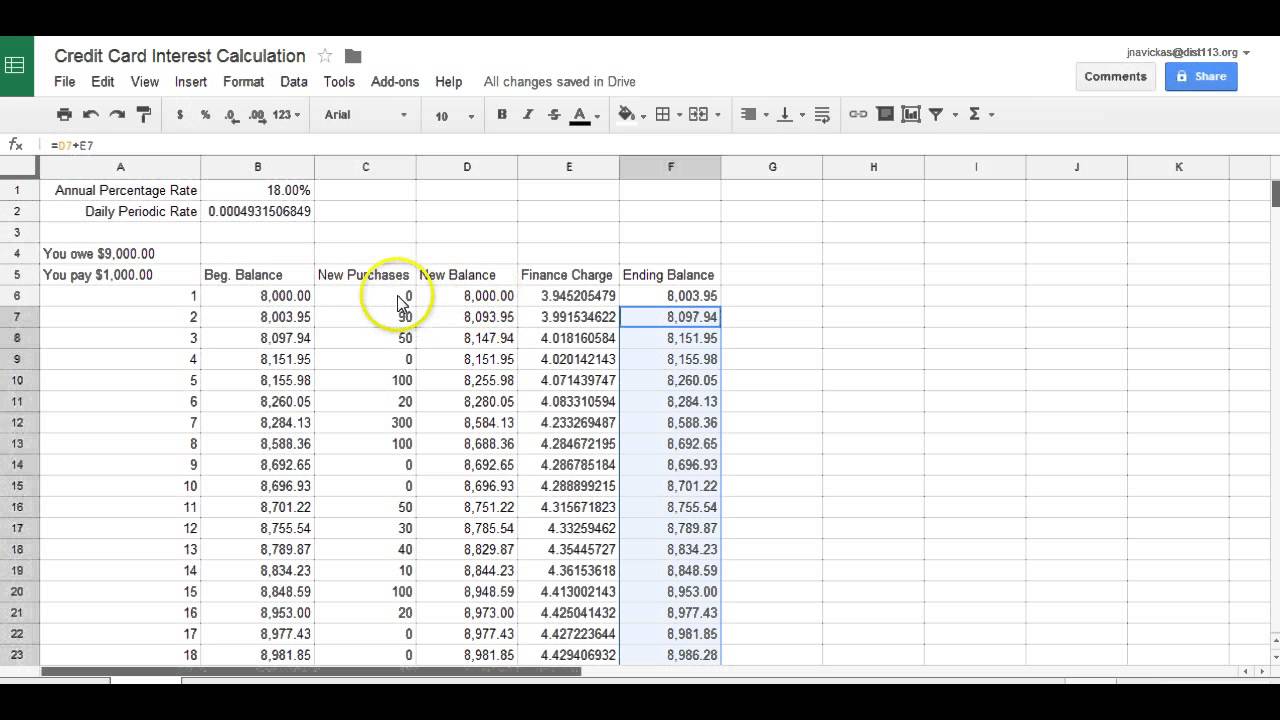

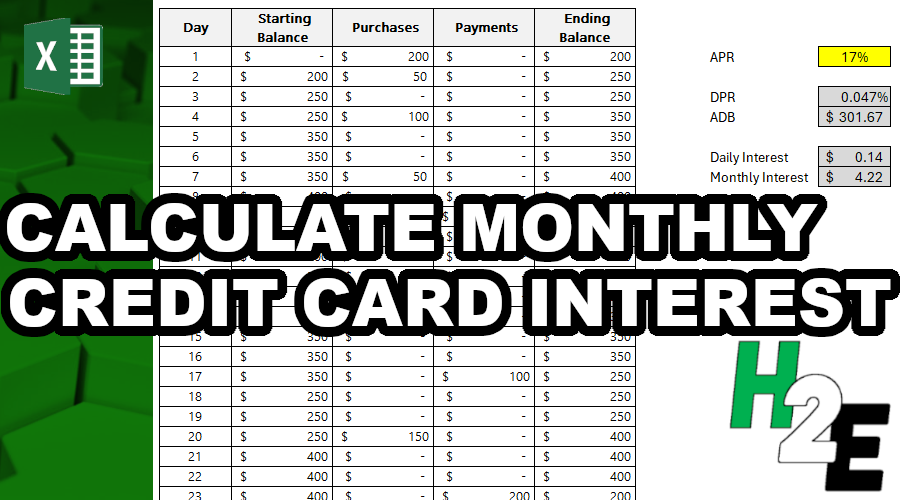

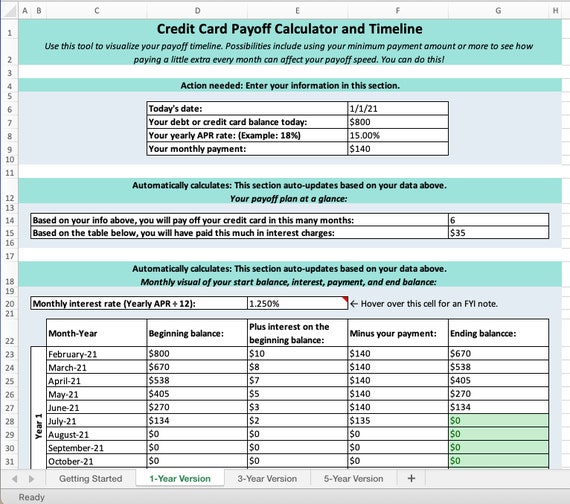

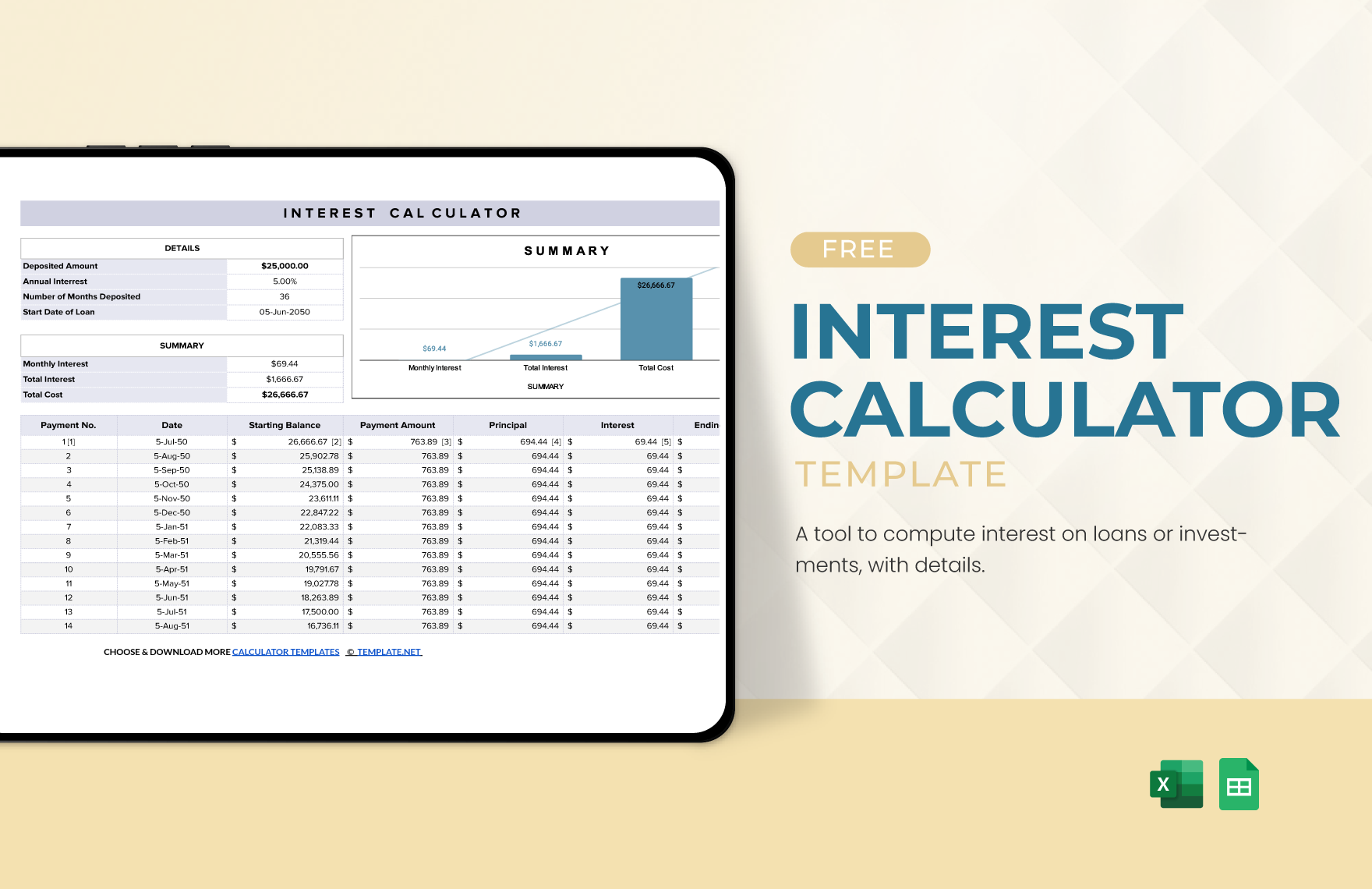

- Amortization Schedule: This is perhaps the most critical feature. It should show a month-by-month breakdown including:

- Starting Balance

- Payment Amount (distinguishing between principal and interest portions)

- Interest Paid

- Principal Paid

- Ending Balance

- Cumulative Interest Paid

- Number of Payments

- Total Interest Paid: A summary of the total amount of interest accrued over the entire repayment period.

- Total Principal Paid: The sum of all principal payments, which should equal the initial balance.

- Total Payments Made: The sum of all monthly payments.

- Debt-Free Date: A clear projection of when the credit card balance will be paid off, assuming consistent payments.

- Interest Savings: Many advanced templates can compare different payment scenarios (e.g., minimum payment vs. desired payment) and highlight the total interest saved by paying more than the minimum.

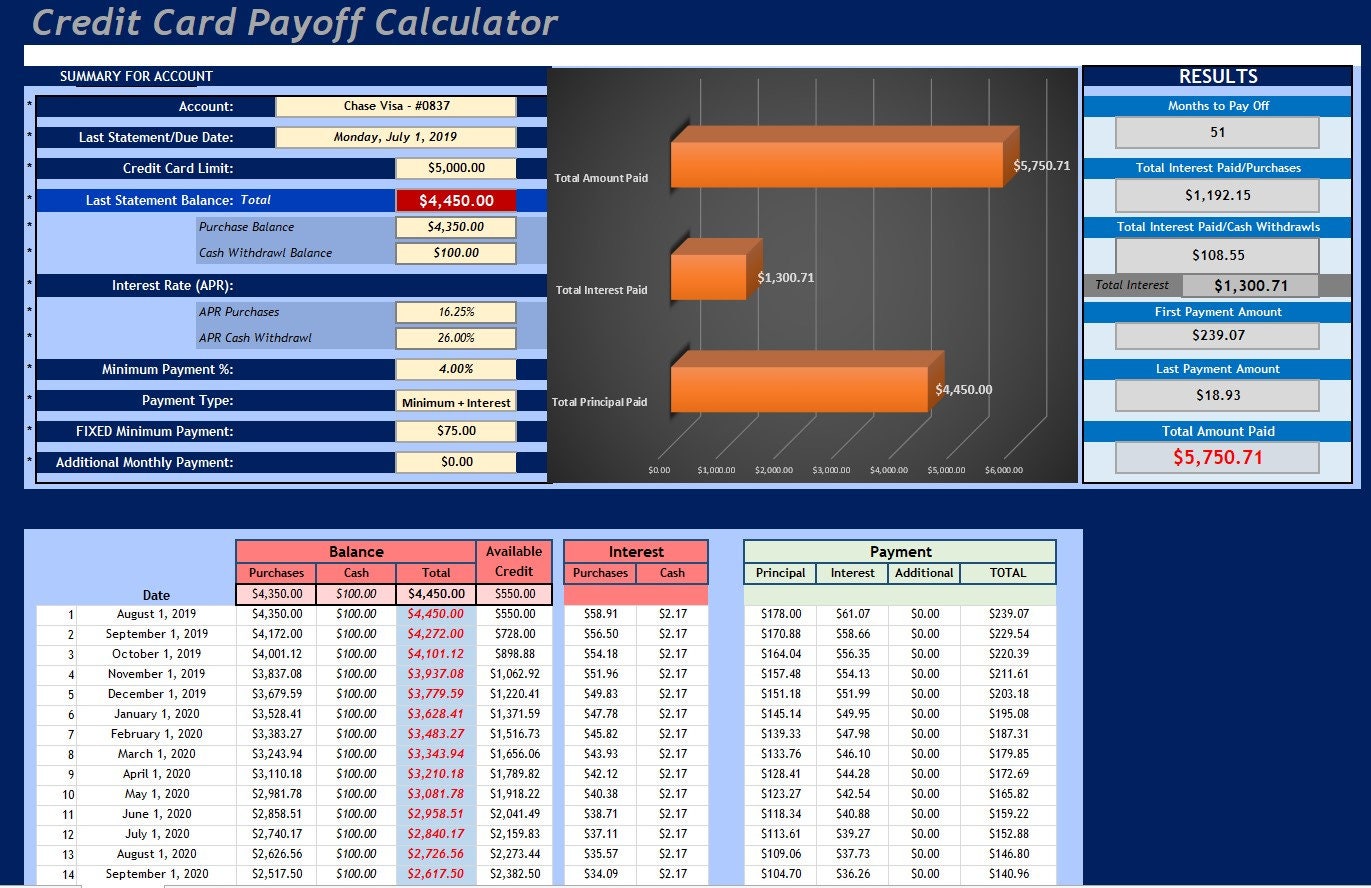

Visualizations and Reporting

Beyond raw numbers, effective templates often incorporate visual elements to make the data more digestible:

- Charts and Graphs: Bar charts showing the breakdown of principal vs. interest for each payment, or line graphs illustrating the decreasing balance over time, can provide powerful visual insights.

- Summary Dashboard: A concise overview of the key metrics (total interest, debt-free date, monthly savings) for quick reference.

These features collectively empower users to not only understand their current debt situation but also to actively plan and strategize for its elimination.

How to Effectively Use Your Credit Card Interest Calculator Excel Template

Once you have a Credit Card Interest Calculator Excel Template, knowing how to leverage it to its fullest potential is key to transforming your financial situation. It's more than just plugging in numbers; it's about strategic analysis and informed decision-making.

Step-by-Step Usage Guide

- Gather Your Data: Before opening the template, collect all necessary information for each credit card you wish to analyze. This includes the current balance, the exact APR, and the minimum payment required. Access your credit card statements or online accounts for accurate figures.

- Input Initial Values: Open your Excel template and carefully enter the gathered data into the designated input fields. Double-check your entries to ensure accuracy, as even small errors can significantly alter the projections.

- Analyze the Minimum Payment Scenario: Initially, use the template to calculate the outcome if you only make the minimum payments. Pay close attention to the

Debt-Free Dateand theTotal Interest Paid. This often serves as a stark wake-up call, highlighting the long-term cost and duration of minimum payments. - Experiment with Higher Payments: This is where the template truly shines. Start incrementally increasing your

Desired Monthly Payment. For example, try adding an extra $25, then $50, then $100 to your minimum payment. Observe how each increase dramatically shortens your repayment period and reduces the total interest paid. - Model Lump Sum Payments: If you anticipate receiving a bonus, tax refund, or any other unexpected income, model the effect of applying a portion or all of it as a lump-sum payment. Many templates allow for this by adjusting the principal balance at a specific point in time, showing the immediate impact on future interest and repayment duration.

- Prioritize Debt (Snowball/Avalanche): If you have multiple credit cards, use individual templates or a master template designed for multiple debts. This allows you to compare different repayment strategies like the debt snowball method (paying off smallest balances first for psychological wins) or the debt avalanche method (paying off highest interest rates first to save the most money). The template will clearly show the financial outcome of each approach.

- Regularly Update and Review: Your credit card balance and possibly your APR can change. Make it a habit to update your template periodically (e.g., monthly) with your latest figures. This keeps your projections accurate and your motivation high as you track your progress towards debt freedom.

Interpreting the Results

Focus on the following key metrics when reviewing your template's output:

- Total Interest Saved: This is often the most compelling number. Seeing how much you can save by slightly increasing your payments can be a huge motivator.

- Accelerated Debt-Free Date: Knowing exactly when you'll be free from a particular credit card debt provides a clear goal to work towards.

- Payment Breakdown: Understanding how much of each payment goes to principal versus interest helps you see your money working more efficiently as the principal portion grows.

By actively engaging with your template and experimenting with different scenarios, you transform it from a simple calculator into a dynamic financial planning tool.

Understanding Credit Card Interest and APR

Before diving deep into using an Excel template, it's crucial to have a solid grasp of how credit card interest works, particularly the Annual Percentage Rate (APR). This foundational knowledge will help you interpret the results from your Credit Card Interest Calculator Excel Template more effectively and make smarter financial decisions.

What is APR?

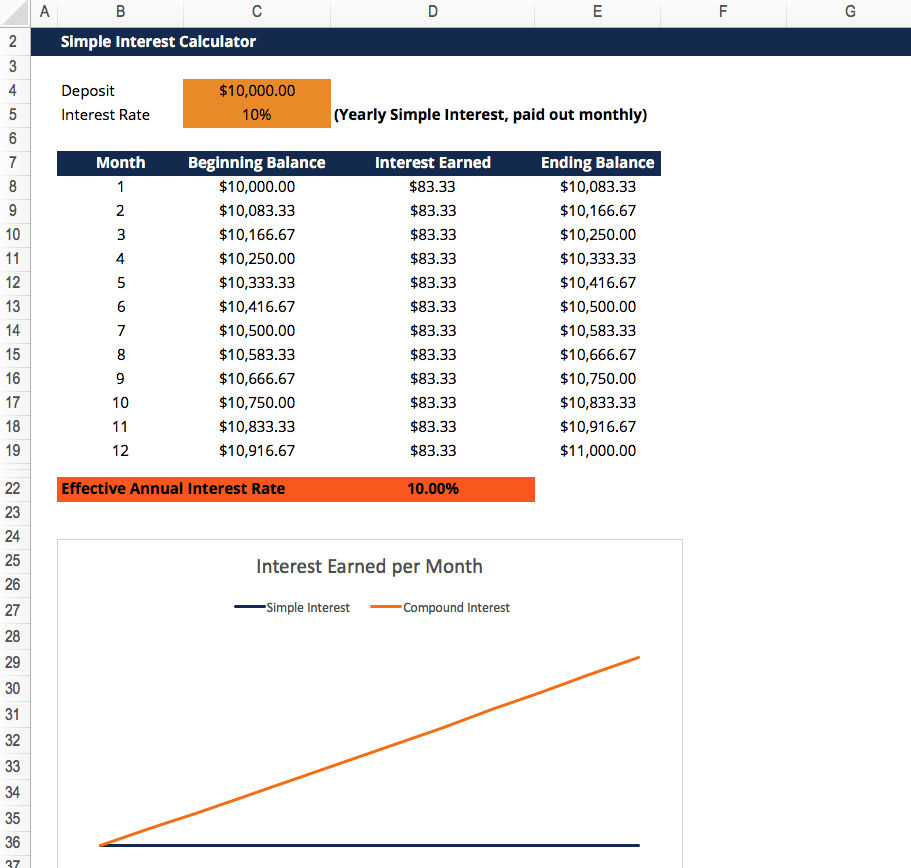

The Annual Percentage Rate (APR) is the yearly interest rate charged on your outstanding credit card balance. It's important to understand that while it's an annual rate, credit card companies typically calculate and apply interest daily or monthly. This means the interest compounds, leading to potentially higher charges than a simple annual calculation might suggest.

Credit card APRs are usually variable, meaning they can change based on an index like the Prime Rate. This fluctuation is why your interest rate isn't always fixed and can impact your repayment schedule. Some cards also have different APRs for purchases, cash advances, or balance transfers, and introductory low APRs that revert to a higher rate after a promotional period. Always use the current, non-promotional APR for your calculations in the Excel template.

How Interest Accrues (Compounding)

Credit card interest compounds, which means that interest is charged not only on your initial balance but also on the accumulated interest from previous periods.

Here's a simplified example of how it typically works:

- Daily Rate: Your APR is divided by 365 (or 360, depending on the issuer) to get a daily periodic rate.

- Average Daily Balance: Your credit card company calculates an average daily balance for your billing cycle. This considers your balance each day, factoring in new purchases, payments, and credits.

- Interest Charge: The daily periodic rate is multiplied by your average daily balance, and then by the number of days in the billing cycle, to determine the total interest charge for that cycle.

- Balance Rollover: This interest charge is then added to your principal balance for the next billing cycle, and new interest will be calculated on this higher amount. This is the essence of compounding.

The longer you carry a balance, and the higher that balance is, the more significant the impact of compounding interest becomes. This is precisely why making only the minimum payment can be so detrimental, as a large portion of that payment often goes straight to interest, barely touching the principal.

The Impact of Minimum Payments

Minimum payments are designed to keep you in debt longer, maximizing the interest revenue for the credit card company. They are typically a small percentage of your outstanding balance (e.g., 1-3%) plus any accrued interest and late fees, or a fixed dollar amount, whichever is greater.

When you only pay the minimum:

- Extended Repayment Time: It can take years, even decades, to pay off a seemingly modest balance.

- Increased Total Cost: Due to compounding interest over such a long period, you end up paying significantly more than the original amount charged.

- Stagnant Principal Reduction: In the early stages of repayment, most of your minimum payment will be consumed by interest, leaving very little to reduce your principal balance.

Using your Credit Card Interest Calculator Excel Template to model minimum payments versus higher payments will vividly illustrate these points, serving as a powerful motivator to prioritize paying down your balances more aggressively.

Customizing and Enhancing Your Excel Template

While a basic Credit Card Interest Calculator Excel Template is incredibly useful, its true power often lies in its adaptability. Excel allows for significant customization, enabling you to tailor the template to your specific financial planning needs and even add advanced features.

Personalizing Your Template

- Visual Aesthetics: Change font styles, colors, and cell formatting to make the template more appealing and easier to read. Highlight key figures like total interest saved or the debt-free date with distinct colors or larger fonts.

- Scenario Labels: If you're comparing multiple payment scenarios (e.g., minimum payment, extra $50, extra $100), add clear labels to each scenario's output. This helps in quickly identifying and comparing different outcomes.

- Adding Notes: Include sections for personal notes or reminders. You might want to jot down the current promotional APR expiry date, specific payment goals, or the dates you plan to review your progress.

Advanced Features You Can Add

For those comfortable with Excel functions and formulas, you can significantly enhance your template's capabilities:

- Multiple Card Aggregation: Create a master sheet that pulls data from individual card calculation sheets. This allows you to manage multiple credit card debts in one place, summarize total debt, and implement strategies like the debt snowball or debt avalanche methods across all your cards. You could even add a column to rank cards by interest rate.

- Extra Payment Schedule: Instead of just a single "desired monthly payment," add a section where you can schedule specific extra payments at different times. For instance, if you know you'll receive a bonus in six months, you can model a lump-sum payment then and see its exact impact.

- Interest Rate Changes: Build in a dynamic field or a simple

IFstatement that allows you to specify a future date when the APR might change (e.g., after an introductory period). This provides a more realistic long-term projection. - "What If" Scenarios with Data Tables: Use Excel's "What If Analysis" tools, specifically

Data Tables, to instantly see how varying two different inputs (e.g., monthly payment and interest rate) affect a single output (e.g., total interest paid). - Conditional Formatting: Apply conditional formatting rules to highlight important cells. For example, you could highlight the month when your balance drops below a certain threshold, or when the interest paid is less than the principal paid in a given month.

- Payment History Tracker: Add columns to record actual payments made against the projected payments. This helps you track your real-world progress and adjust future projections as needed, providing a more robust Credit Card Interest Calculator Excel Template.

By taking the time to customize and enhance your template, you'll create a powerful, personalized tool that goes beyond simple calculations, offering deeper insights and greater control over your credit card debt management.

Tips for Managing Credit Card Debt

Using a Credit Card Interest Calculator Excel Template is an excellent step towards managing your debt, but it's part of a larger strategy. Here are some actionable tips to help you reduce and eventually eliminate your credit card debt:

1. Create and Stick to a Budget

The most fundamental step in debt management is understanding where your money goes. Create a detailed budget that tracks all your income and expenses. Identify areas where you can cut back, even small amounts, to free up more money for debt repayment. Tools like your Excel template can help you visualize how even an extra $25 or $50 a month can make a significant difference.

2. Prioritize High-Interest Debt (Debt Avalanche)

Your Excel template can clearly show you which credit card is costing you the most in interest. The debt avalanche method involves paying the minimum on all cards except the one with the highest APR, on which you pay as much extra as possible. Once that card is paid off, you roll that payment amount into the next highest APR card, and so on. This method saves you the most money on interest over time.

3. Consider the Debt Snowball Method

Alternatively, the debt snowball method prioritizes paying off the smallest balance first, regardless of the interest rate. Once that card is paid off, you take the money you were paying on it and add it to the payment of the next smallest debt. This method provides psychological wins early on, which can be highly motivating for some individuals, helping them stay committed to their debt repayment journey. Your template can model both to see which feels more achievable for you.

4. Negotiate Lower Interest Rates

It never hurts to ask! Call your credit card companies and ask if they would consider lowering your APR, especially if you have a good payment history. Even a small reduction can save you a significant amount of money and shorten your repayment time, which your Credit Card Interest Calculator Excel Template can instantly verify.

5. Consolidate Debt (Carefully)

If you have multiple high-interest debts, consider consolidating them into a single, lower-interest payment through a balance transfer credit card (with a 0% introductory APR) or a personal loan. Be very cautious with balance transfers; ensure you can pay off the balance before the promotional rate expires, or you could end up with even higher interest. Always calculate the total cost with your Excel template before making such a move.

6. Avoid New Debt

While aggressively paying down existing debt, it's crucial to avoid accumulating new debt. Cut up or freeze your credit cards if necessary, and commit to only spending money you actually have. This prevents the "two steps forward, one step back" scenario.

7. Build an Emergency Fund

Having a small emergency fund (e.g., $1,000) can prevent you from relying on credit cards for unexpected expenses. This crucial step ensures that your progress in debt repayment isn't derailed by life's surprises.

By combining the analytical power of a Credit Card Interest Calculator Excel Template with these strategic debt management tips, you create a comprehensive plan to achieve financial freedom.

Conclusion

Taking control of credit card debt is a journey that requires both discipline and the right tools. A Credit Card Interest Calculator Excel Template emerges as an indispensable resource, transforming the often-confusing landscape of credit card interest into a clear, actionable roadmap. It empowers individuals to move beyond simply making minimum payments, offering the transparency, flexibility, and insights needed to strategically attack debt.

Throughout this article, we've explored the manifold benefits of using such a template, from gaining a clear understanding of interest accrual to visualizing accelerated debt repayment scenarios. We've delved into the essential features that make these templates so effective, including detailed amortization schedules and powerful projection capabilities. Furthermore, we've provided a step-by-step guide on how to maximize your template's utility, alongside crucial tips for interpreting the data and understanding the mechanics of APR and compounding interest. Finally, we touched upon customizing your template to fit your unique financial situation and integrating it into a broader debt management strategy.

By harnessing the power of a customized Excel template and coupling it with sound financial practices, you're not just calculating numbers; you're building a personalized path to financial freedom. This proactive approach will not only save you thousands in interest but also provide the confidence and clarity needed to master your credit card debt, paving the way for a more secure financial future.

0 Response to "Credit Card Interest Calculator Excel Template"

Posting Komentar