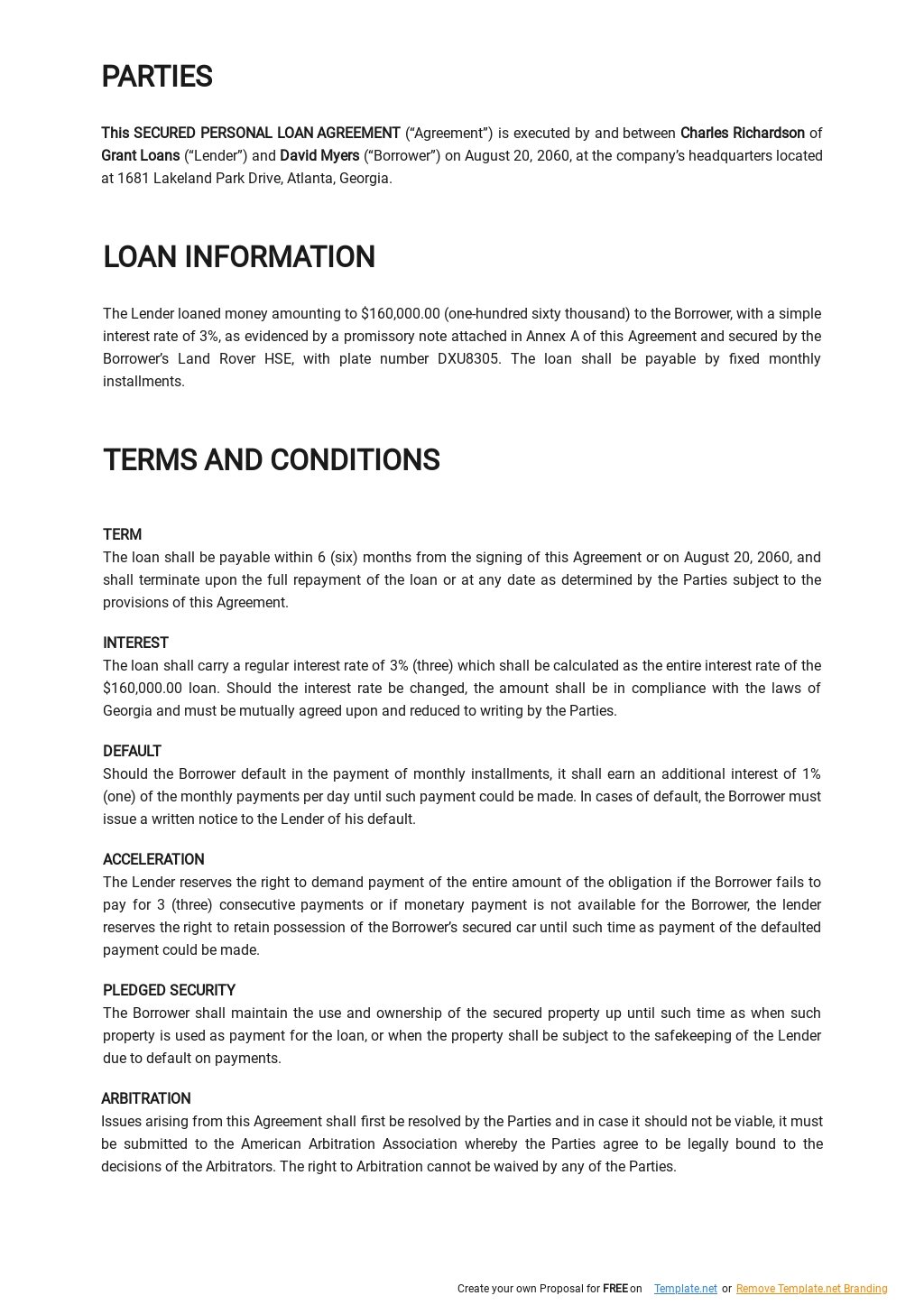

Creating a legally sound and secure promissory note is a critical step in any business relationship. It's a document outlining the terms of a loan, ensuring both parties are protected and clearly defined. A properly drafted secured promissory note provides a robust framework for managing financial obligations and minimizing potential disputes. This guide will delve into the essential components of a secured promissory note, offering a comprehensive overview for businesses and individuals alike. Understanding the nuances of this document is paramount for safeguarding your financial interests. The core principle of a secured promissory note is that the lender has a claim on the borrower's assets if the borrower defaults on the loan. This provides a significant layer of security for the lender. A well-structured note protects both the lender and the borrower, fostering trust and stability within the business relationship. This article will explore the key elements, best practices, and potential pitfalls associated with creating and utilizing a secured promissory note.

Understanding the Importance of a Secured Promissory Note

Before diving into the specifics, it's vital to grasp why a secured promissory note is so important. It's far more than just a simple loan agreement. It's a legally binding contract that establishes a clear path for repayment. The lender's security interest in the borrower's assets – such as accounts receivable, inventory, or equipment – provides a powerful incentive to ensure the borrower fulfills their obligations. Without this security, the lender faces a significantly higher risk of loss if the borrower fails to repay. Furthermore, a secured note often facilitates easier access to funds for the borrower, as the lender can seize and sell the collateral to recover their investment. The process of securing a note can also streamline the loan disbursement, reducing administrative burdens and accelerating the flow of capital. A properly executed secured promissory note is a cornerstone of sound financial management.

Key Components of a Secured Promissory Note

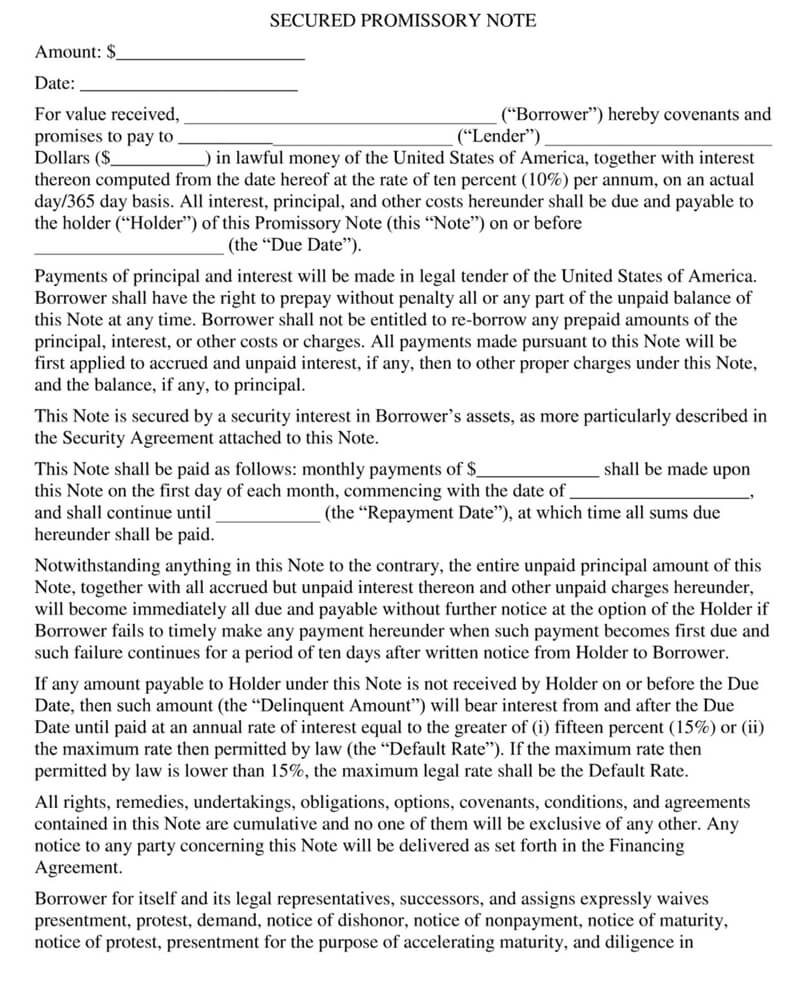

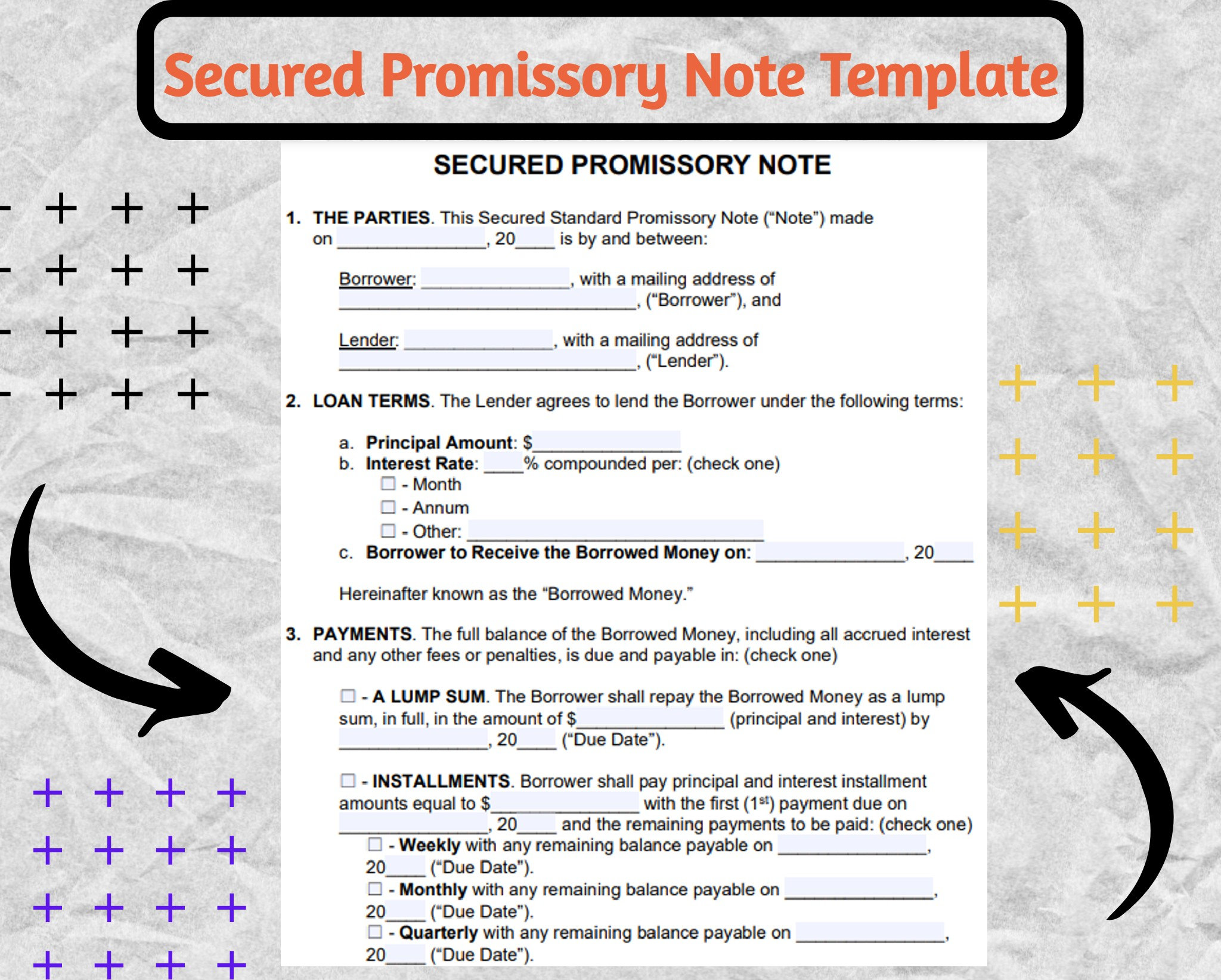

A comprehensive secured promissory note typically includes the following key elements:

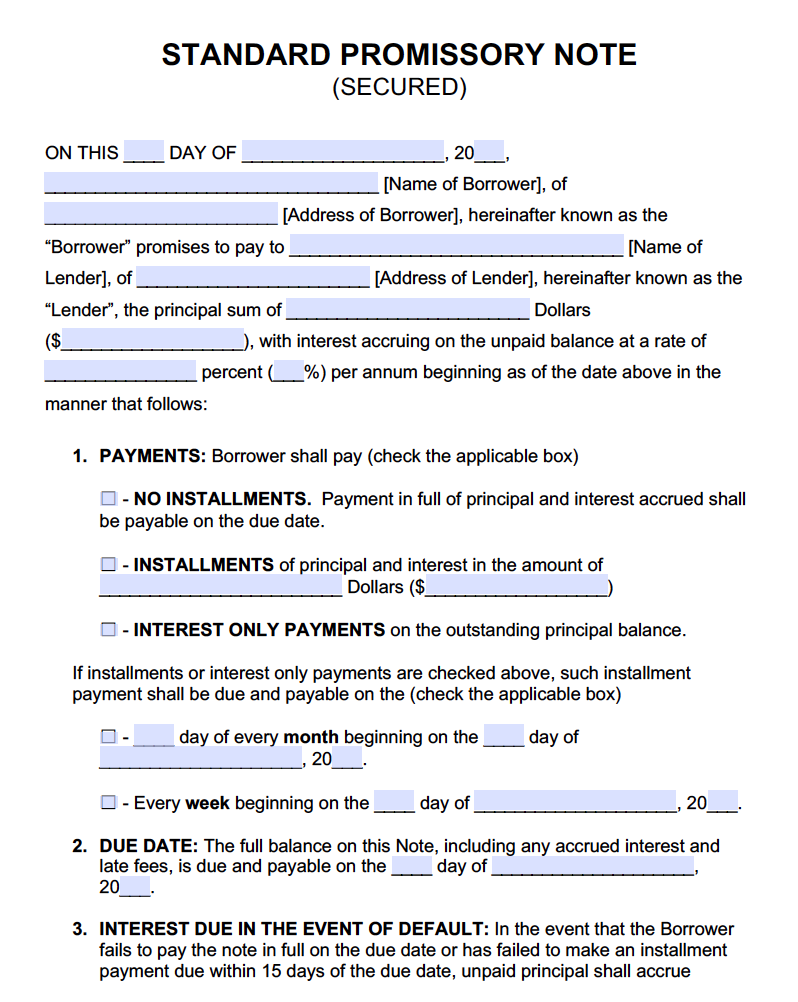

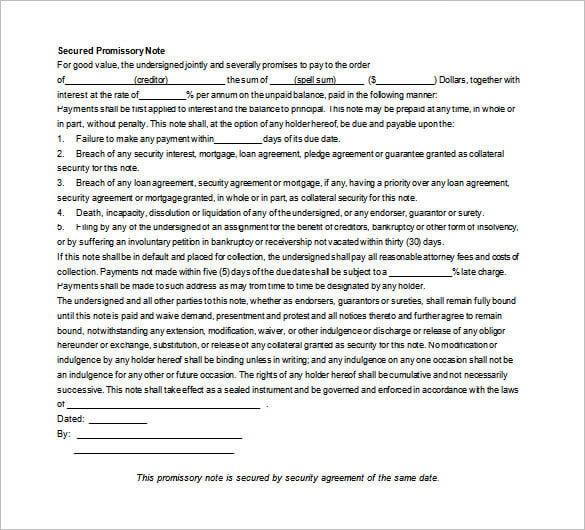

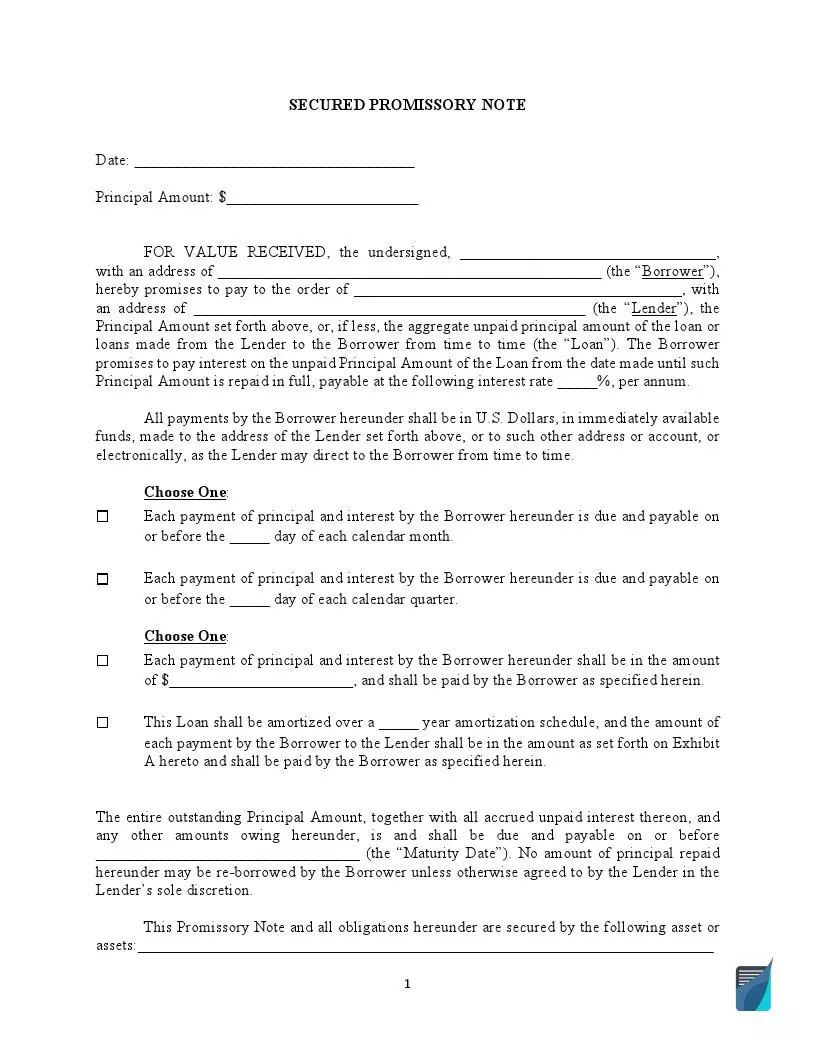

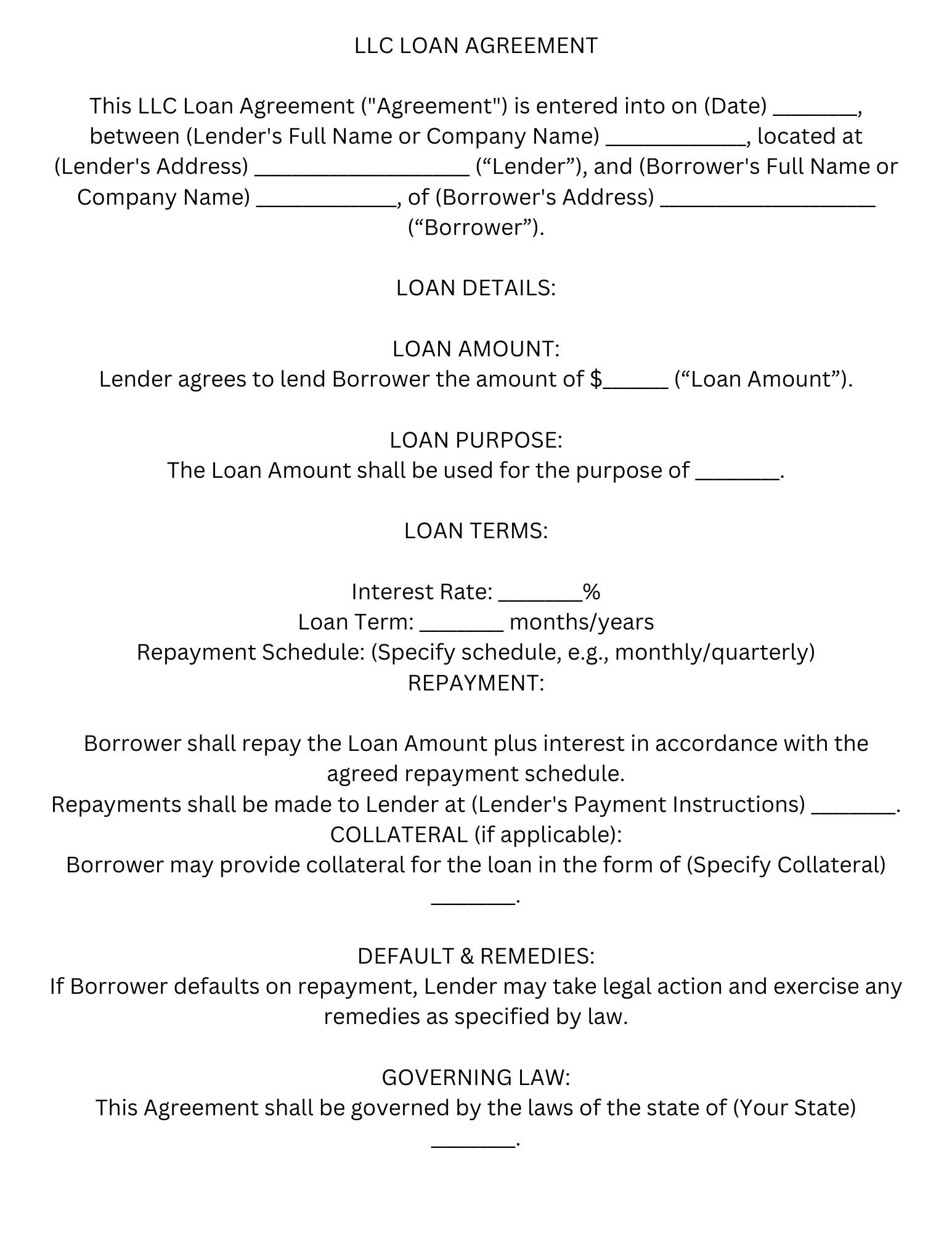

- Parties Involved: Clearly identify the borrower and the lender. This includes full legal names, addresses, and contact information.

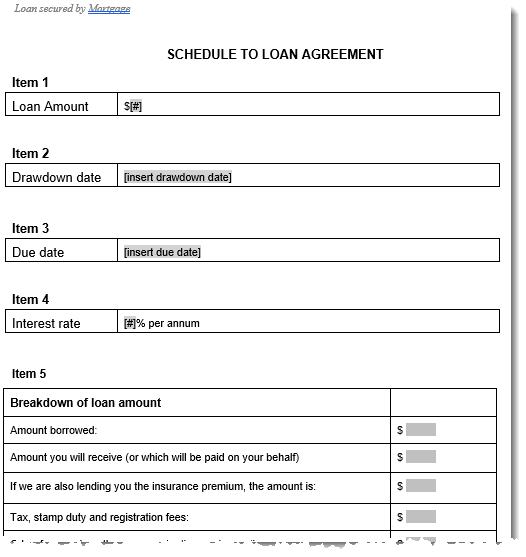

- Loan Amount: Specify the exact amount of the loan being requested.

- Interest Rate: Define the interest rate, whether fixed or variable, and the payment schedule.

- Repayment Schedule: Outline the exact dates and amounts of each payment. This includes the frequency of payments (e.g., monthly, quarterly) and the total repayment period.

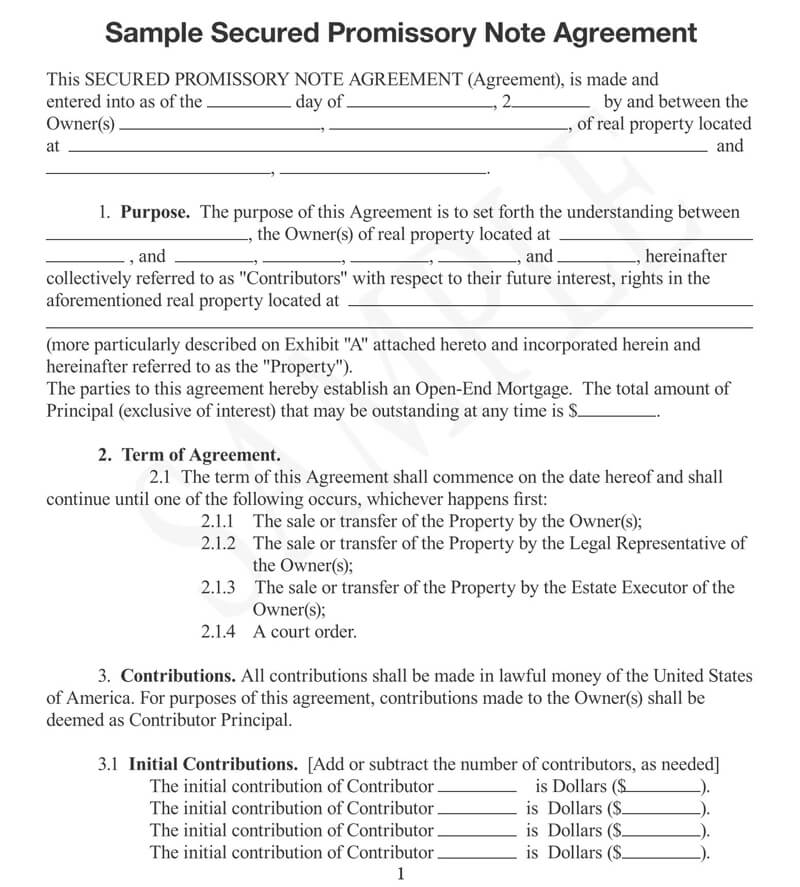

- Collateral: Detail the specific assets pledged as collateral. This is a crucial section and requires careful consideration of the value and liquidity of the pledged items.

- Default Provisions: Define the consequences of default, including penalties and potential legal action.

- Governing Law: Specify the jurisdiction whose laws will govern the agreement.

- Amendment Clause: Include a clause outlining how the note can be amended or modified in the future.

The Role of Collateral in a Secured Promissory Note

The collateral component is arguably the most important aspect of a secured promissory note. It represents the assets that the lender has a claim on if the borrower defaults. The value of the collateral should be sufficient to cover the outstanding loan amount. Common types of collateral include:

- Accounts Receivable: Money owed to the borrower by their customers.

- Inventory: Goods held by the borrower for sale.

- Equipment: Machinery, vehicles, or other equipment used by the borrower.

- Real Estate: Land or buildings owned by the borrower.

- Secured Personal Property: Items like jewelry or artwork that are pledged as collateral.

It's essential to accurately assess the value and liquidity of the collateral to ensure it provides adequate protection for the lender. The lender should also consider the potential for depreciation of the collateral over time. Proper valuation and documentation are critical for a successful collateral arrangement.

Securing a Promissory Note: Strategies and Considerations

Several strategies can be employed to secure a promissory note, each with its own advantages and disadvantages:

- Cash Collateral: This is the simplest and most common method, involving readily available cash as collateral.

- Accounts Receivable Collateral: This involves securing the loan by promising to pay the lender the outstanding receivables.

- Inventory Collateral: This is suitable for businesses that hold inventory.

- Equipment Collateral: This is appropriate for businesses with valuable equipment.

- Personal Property Collateral: This is used for items like jewelry or artwork, requiring careful appraisal.

The choice of collateral will depend on the specific circumstances of the loan and the borrower's business. It's crucial to consult with legal counsel to determine the most appropriate collateral strategy. Furthermore, the lender should carefully evaluate the risk associated with each type of collateral.

The Importance of Legal Review and Professional Assistance

Creating and executing a secured promissory note requires careful attention to detail and adherence to legal requirements. It is strongly recommended to engage a qualified attorney to draft and review the note. An attorney can ensure that the note complies with all applicable laws and regulations, protects the borrower's interests, and minimizes the risk of disputes. They can also advise on the appropriate collateral strategy and negotiate favorable terms with the lender. Errors or omissions in the note can have significant legal consequences, so professional assistance is invaluable.

Understanding Loan-to-Value (LTV)

Loan-to-Value (LTV) is a critical metric used in secured lending. It represents the ratio of the loan amount to the value of the collateral. A lower LTV indicates a greater security for the lender, as the borrower has a smaller portion of their assets at risk. Lenders typically prefer LTVs below 70%, although this can vary depending on the industry and the specific loan terms. A higher LTV increases the lender's risk, but it can also lead to a lower interest rate. Accurate LTV calculations are essential for determining the appropriate interest rate and terms of the loan.

Due Diligence for Lenders

Lenders conduct thorough due diligence before approving a secured promissory note. This involves examining the borrower's financial statements, credit history, and business operations. They will assess the borrower's ability to repay the loan and the value of the collateral. Key areas of due diligence include:

- Financial Statements: Reviewing the borrower's balance sheet, income statement, and cash flow statement.

- Credit Report: Examining the borrower's credit history to assess their creditworthiness.

- Business Plan: Analyzing the borrower's business plan to understand their operations and growth potential.

- Collateral Valuation: Confirming the value and liquidity of the collateral.

- Legal Compliance: Ensuring the borrower complies with all applicable laws and regulations.

Comprehensive due diligence minimizes risk and strengthens the lender's position in the loan transaction.

Common Pitfalls to Avoid

Several common pitfalls can arise when creating and utilizing a secured promissory note. It's important to be aware of these pitfalls to avoid costly mistakes:

- Insufficient Collateral: Not pledging enough collateral to adequately protect the lender.

- Inaccurate Valuation: Overvaluing or undervaluing the collateral.

- Lack of Legal Review: Failing to engage a qualified attorney.

- Ambiguous Language: Using unclear or ambiguous language in the note.

- Failure to Comply with Regulations: Not adhering to all applicable laws and regulations.

Addressing these potential pitfalls proactively can significantly improve the success of the secured promissory note.

The Future of Secured Promissory Notes

The secured promissory note market is expected to continue to grow as businesses increasingly rely on this type of financing. Technological advancements, such as blockchain, are also likely to play a role in streamlining the process of creating and managing secured notes. Increased regulatory scrutiny regarding loan disclosures and security requirements will also shape the industry. The focus will increasingly be on creating more efficient and transparent processes, ensuring that borrowers and lenders can confidently engage in these critical financial agreements.

Conclusion

Secured promissory notes are a powerful tool for businesses and individuals seeking to secure financing. By understanding the key components, risks, and best practices associated with this document, you can create a legally sound and effective agreement that protects your interests and fosters a strong financial relationship. Remember to prioritize legal counsel and thorough due diligence to ensure the success of your secured promissory note. The secure nature of this agreement provides a crucial layer of protection, contributing to stability and long-term financial health. Investing in a well-structured secured promissory note is an investment in your future.

0 Response to "Secured Promissory Note Template"

Posting Komentar